A More Positive 2023

Stocks continued to move higher last week, with the Dow back above 34,000 and officially closing at a new seven-month high along the way. After energy led the rally, several other sectors, including financials, health care, materials, and industrials are now participating and showing strength. This is encouraging and makes us more confident with our call that the bear market ended in mid-October.

- We’re moving into a period that is traditionally strong for equities.

- The consumer still looks healthy, and easing inflation will help.

- Minutes from the Federal Reserve’s last meeting suggest the pace of rate hikes will slow.

- Recession odds are higher, but that is not our base case.

More to consider as we head into 2023:

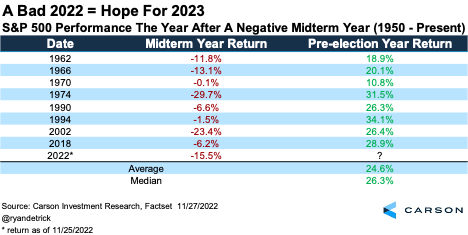

- Year three of the presidential cycle (also called a pre-election year) is the best for stocks, with the S&P 500 up 16.8% on average since 1950.

- Of the past 13 recessions, not one started in a pre-election year.

- When the S&P 500 has closed lower during a midterm year (such as will likely happen this year), it was higher the following year every time (8 for 8) and up a very impressive 24.6% on average since 1950.

A Healthy Consumer

Last week, a strong retail sales report boosted economic growth expectations for the fourth quarter. But the big question is whether consumer spending will remain strong in 2023. This is important because consumption, or lack thereof, will determine whether the U.S. will experience a recession over the next 12 months. Consumer spending accounts for 70% of GDP, so that’s pretty much the ball game. We believe the consumer is in a strong position for several reasons.

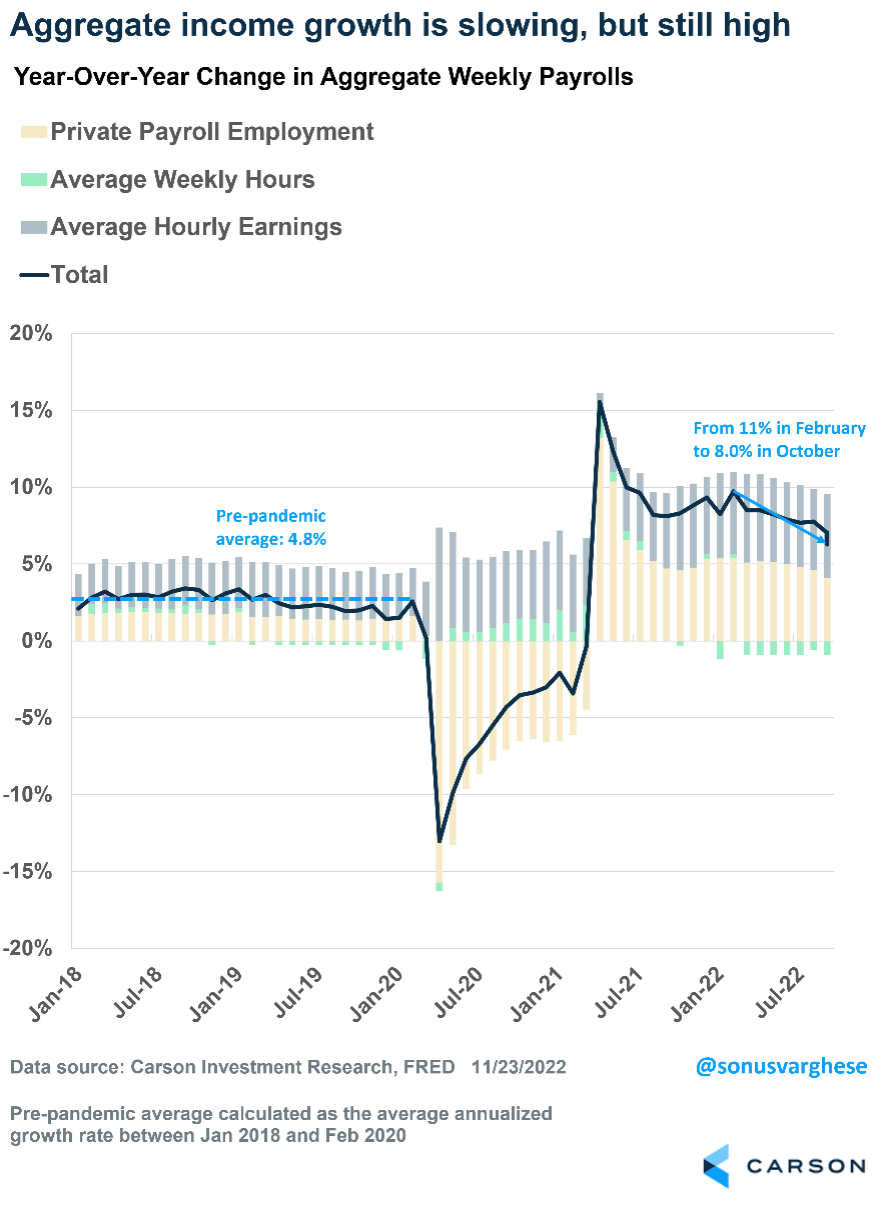

Most consumers spend out of their wages, so it helps to look at overall income in the economy. The chart below shows the year-over-year growth in aggregate weekly earnings, i.e., weekly earnings across all workers, which can be attributed to three sources:

- Employment growth: As more people become employed, overall income in the economy increases, driving more spending. Employment growth has been strong recently.

- Hours worked: As people work more, they earn more and overall incomes go up. The number of hours worked has been falling in recent months, but that’s mostly a reversal from the significant jump during the pandemic.

- Average hourly earnings: As workers earn more, overall incomes go up. Average hourly earnings have been hot over the past year, but they have slowed recently.

Aggregate earnings growth has slowed this year, from 11% to 8%. However, it is still higher than the pre-crisis pace of just under 5%. Employment growth will likely slow in 2023. Payroll gains have averaged about 289,000 over the past three months, but even half that number would create solid income growth comparable to pre-pandemic levels.

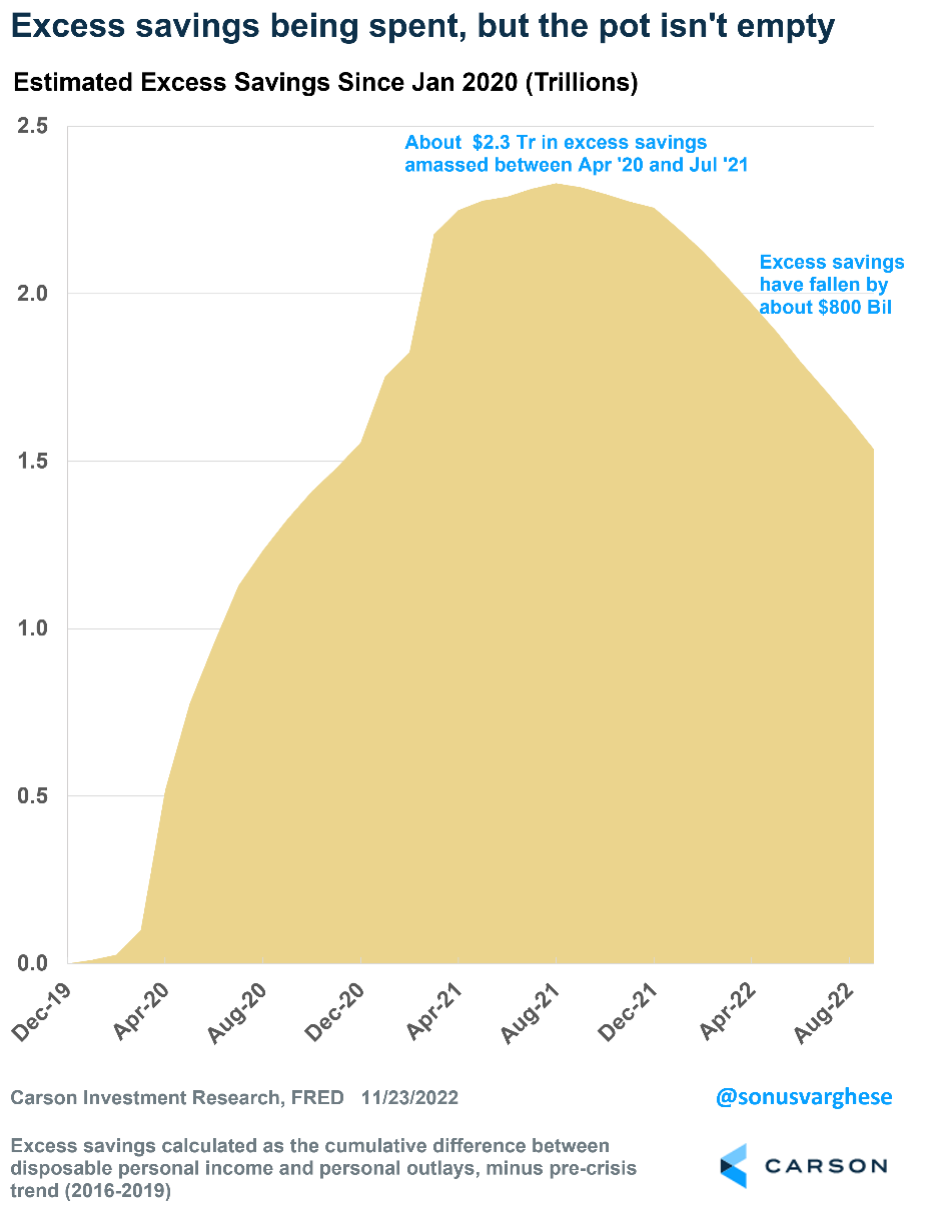

Consumers Still Have Excess Savings

Between April 2020 and July 2021, consumers saved an estimated $2.3 trillion over and above the pre-crisis trend. Much was due to fiscal policy, such as stimulus checks and expanded unemployment benefits. However, for the top 25% of earners, it was almost entirely due to reduced spending amid the pandemic.

Over the past year, consumers have drawn down these excess savings by an estimated $800 billion. But savings are still high.

Most of these excess savings are held by the top 50% of income earners. Inflation tends to hit lower-income workers harder, which means they probably had to draw on more of their excess savings to fund purchases.

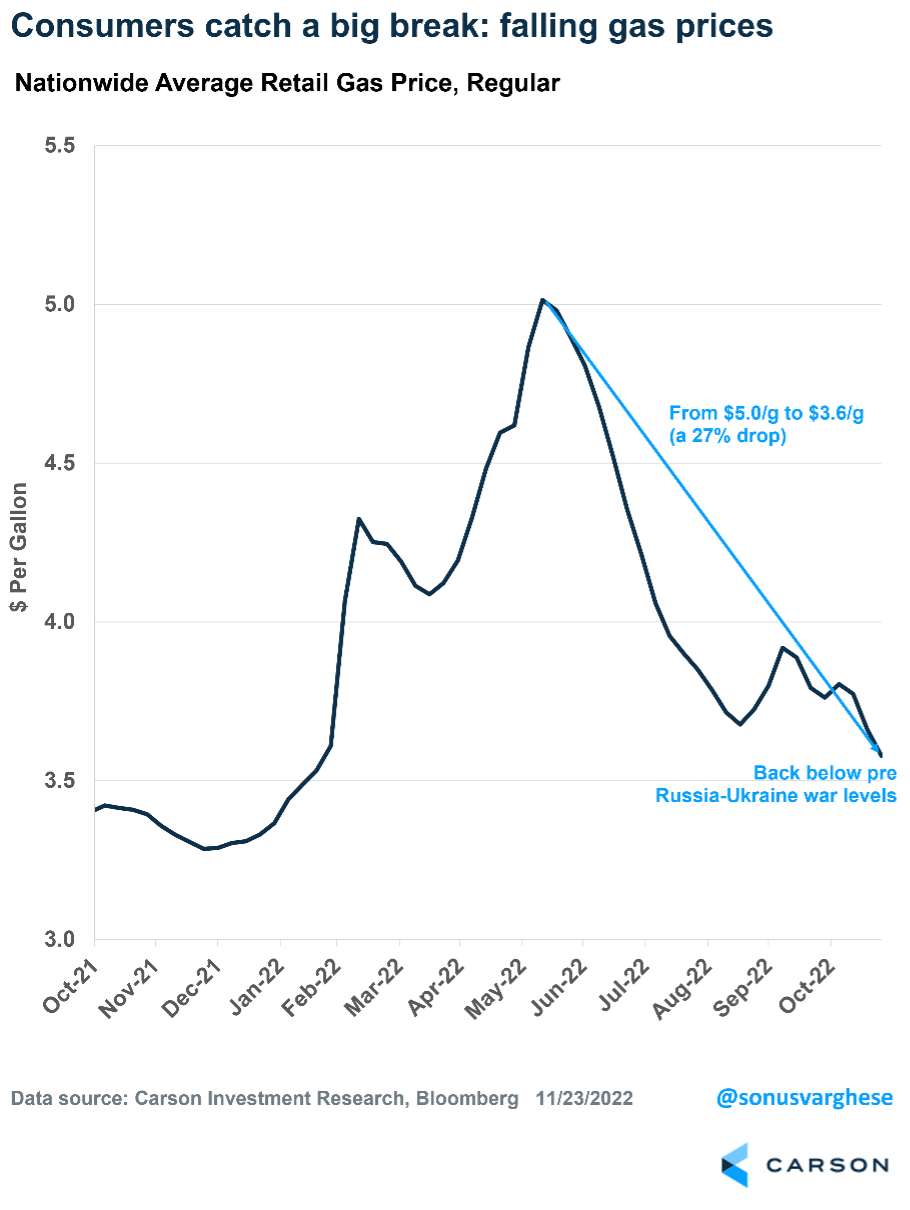

But the consumer got a big break recently in the form of retreating gas prices. Gas prices are now almost back to where they were on the eve of Russia’s invasion of Ukraine. In a sense, just like higher gas prices were effectively a tax on incomes, falling gas prices are akin to a tax cut.

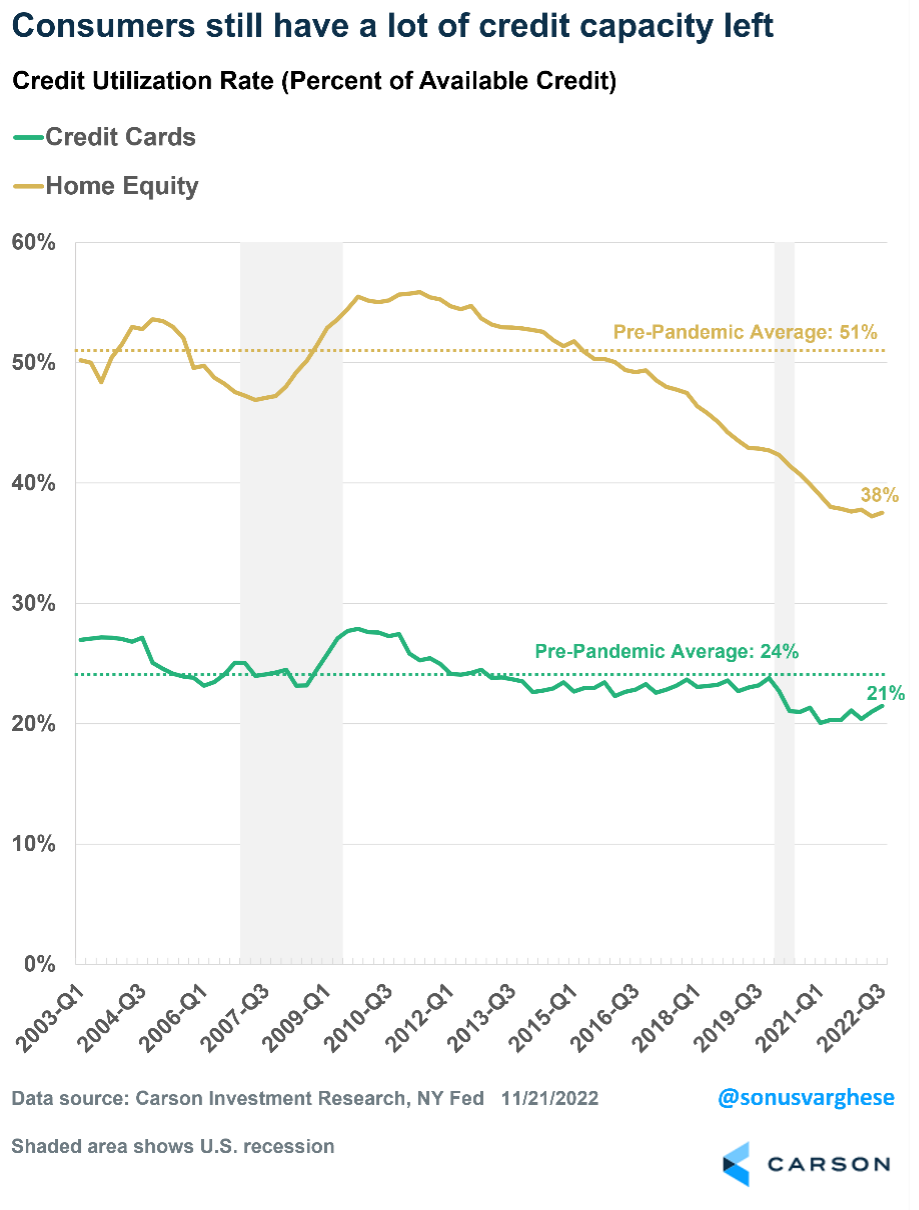

Consumers Still Have Borrowing Capacity

Credit card spending is rising, which is not surprising. Prices are higher and consumers are spending more (even adjusted for prices). But more important than total debt is the debt service burden for households, which is close to record lows. The chart below shows households’ debt service as a percent of disposable income. As of the end of the second quarter, this metric was at 9.6%, well below the pre-pandemic average of 11.2%.

Also, credit utilization rates are still low. Consumers have yet to tap into their credit cards and home equity lines of credit to the same extent as before the pandemic hit. Utilization rates are also well below average levels over the past few decades.

Easing Inflation is Positive for Consumers

Excess savings were drawn down this year because income gains were not keeping up with prices. But as inflation eases, real incomes will likely start rising again, and the rate at which that excess savings pot gets depleted should slow down.

Of course, the other side of more robust real incomes is that demand will be strong, which could keep inflation on the higher side. However, we on the Carson Investment Research Team believe inflation will ease due to idiosyncratic downward pressure, as the same forces that boosted inflation reverse.

This should ease pressure on the Fed, and it looks like Fed members are recognizing that they’ve already done a lot by raising rates as much as they have. Minutes from the Fed’s November meeting suggest most officials favor a slowdown in the pace of interest rate increases.

All in all, the consumer is in a good position as we go into 2023, raising the likelihood that consumption will remain strong over the next year — and that should help avoid a recession despite the rapid pace of interest rate hikes in 2022.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

Ryan is a non-registered associates of Cetera Advisor Networks.

Compliance Case # 01565296