After the best week of the year for stocks two weeks ago, it was nice to see some follow-through last week. We think the stage is set for a strong end-of-year rally and the late-October lows won’t be violated. November and December are historically two of the strongest months. And even more encouragingly, when stocks are positive heading into November, markets tend to chase year-to-date strength as investment managers add equities before the year’s close.

STOCK MARKET

- Stocks gained last week, after they had their best week of the year.

- Improving earnings and profit margins may be a major tailwind for equities next year.

ECONOMY

- The economy saw blockbuster productivity growth in the third quarter.

- Business formation and policy could continue to support productivity in 2024.

STOCK MARKET: WHY WE THINK THE BULL MARKET WILL CONTINUE IN 2024

https://www.averywealth.com/wp-admin/media-upload.php?post_id=66525&type=image&TB_iframe=1https://www.averywealth.com/wp-admin/media-upload.php?post_id=66525&type=image&TB_iframe=1

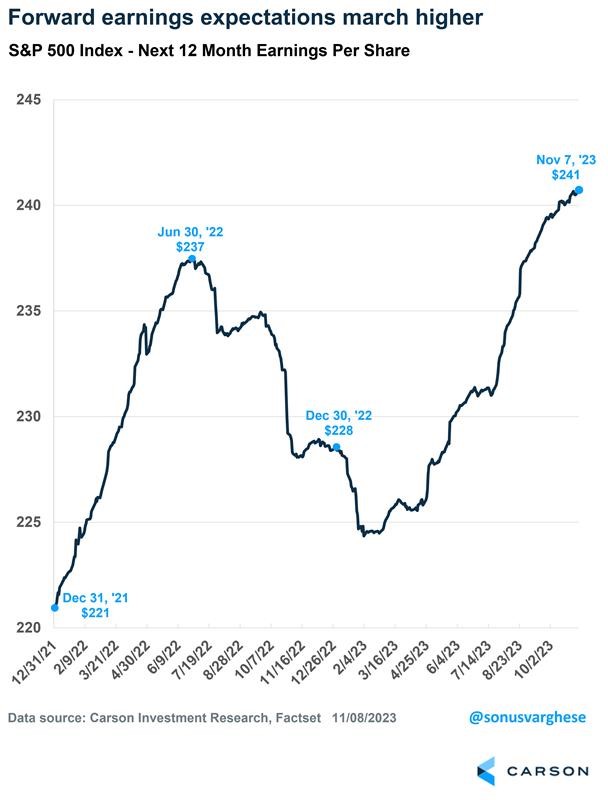

As we head into 2024, earnings could drive stocks higher. Analysts continue to come in too low on estimates at the start of earnings season. The third quarter was expected to finish with earnings slightly down over the trailing year, but S&P 500 earnings are now expected to gain 4% and analysts predict record profits over the next 12 months. When profits are at a record, stocks tend to follow, and we expect that to occur in 2024.

Even more surprising than record profits is improved profit margins. Over the past year, we have heard frequently that profit margins are too high and must fall. Since March, forward 12-month profit margins have increased. If both profits and profit margins increase next year, equities should have a substantial tailwind.

ECONOMY: PRODUCTIVITY GROWTH COULD BE A GAME CHANGER

Lost in all the consternation over a weak payroll report this month was robust productivity data, which was released earlier. Labor productivity rose at an annualized pace of 4.9% in the third quarter. This is not entirely surprising because we knew output surged during the quarter and hours worked didn’t change significantly. In short, private sector workers across the economy produced a significantly higher amount of output without substantially increasing the amount of time they worked in aggregate. This kind of productivity strength, if it continues, can have big implications.

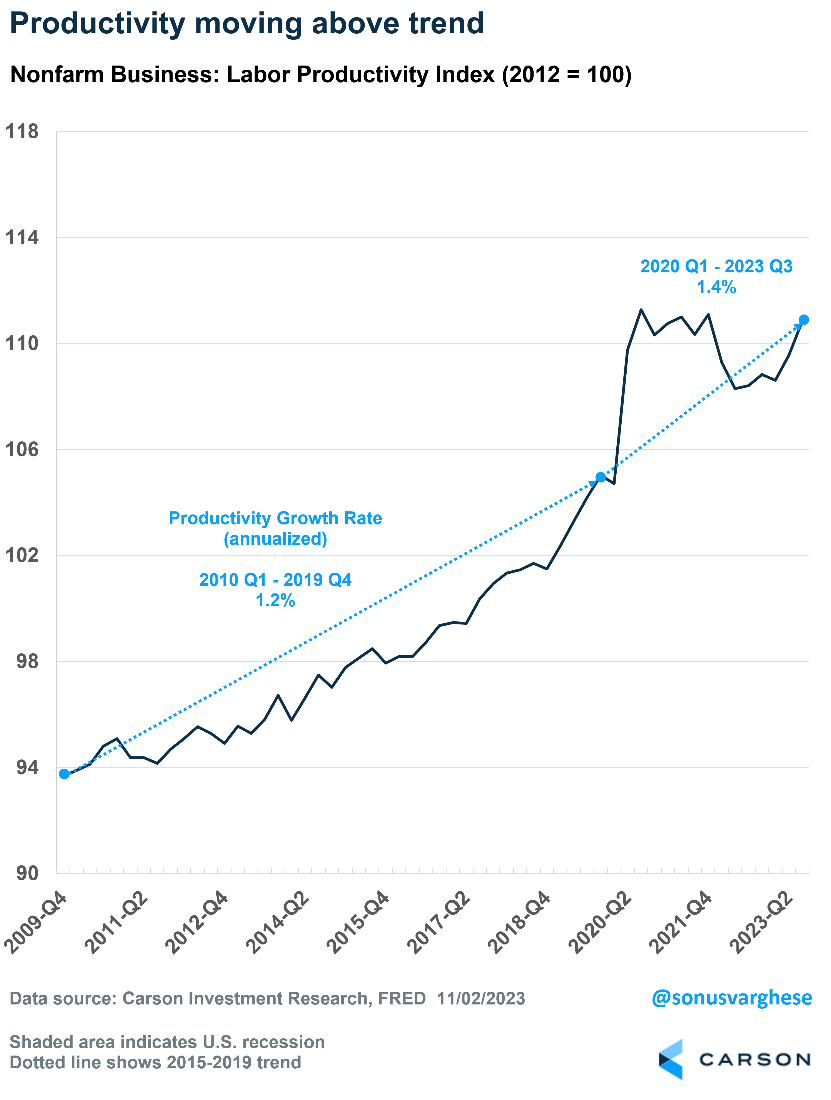

The third quarter’s blockbuster productivity data follows a hot number from the prior quarter, when productivity rose 3.5% (annualized). Quarterly productivity data can be quite noisy, so it helps to broaden the horizon. Since 2020, productivity has averaged a 1.4% annual pace, which is faster than the 2010-2019 pace of 1.2%.

Productivity surged after the pandemic hit. Economic output regained its pre-pandemic level by the first quarter of 2021, with 8 million fewer workers, which translated to higher productivity per worker. But this was not because the productive capacity of the economy expanded. Workers can be squeezed for a time to produce more amid downsizing — the same thing has happened amid prior recessions. But it lasts only for so long.

Productivity subsequently fell in 2022, “reversing” the gains from 2020-2021. As workers were rehired, it looked like productivity was falling. Newly hired workers had to be trained, or re-trained, and periods like these are not great for productivity growth.

But now that the economy is normalizing, all the investment over the last couple of years is bearing fruit (including investment in labor), and productivity is accelerating. Over the last two quarters, productivity growth has run at a 4.1% annualized pace, which is the fastest two-quarter pace outside of recessions and immediate post-recession periods since the late 1990s.

Higher Productivity is a Big Deal for the Economy and Inflation

Wage growth for workers is essentially the sum of productivity growth, inflation, and the change in labor’s share of income. Faster wage growth implies some combination of:

- faster productivity growth;

- higher inflation; or

- an increase in the share of output going to labor (instead of profits).

All three elements do not have to occur at once. In other words, productivity growth can support higher wages without higher inflation.

Higher wages can result from higher productivity in any number of ways, including businesses introducing more machines or organizing work more efficiently. Workers can also be more incentivized to be more efficient. Higher wages can also force less productive firms out of business, raising overall productivity across the economy.

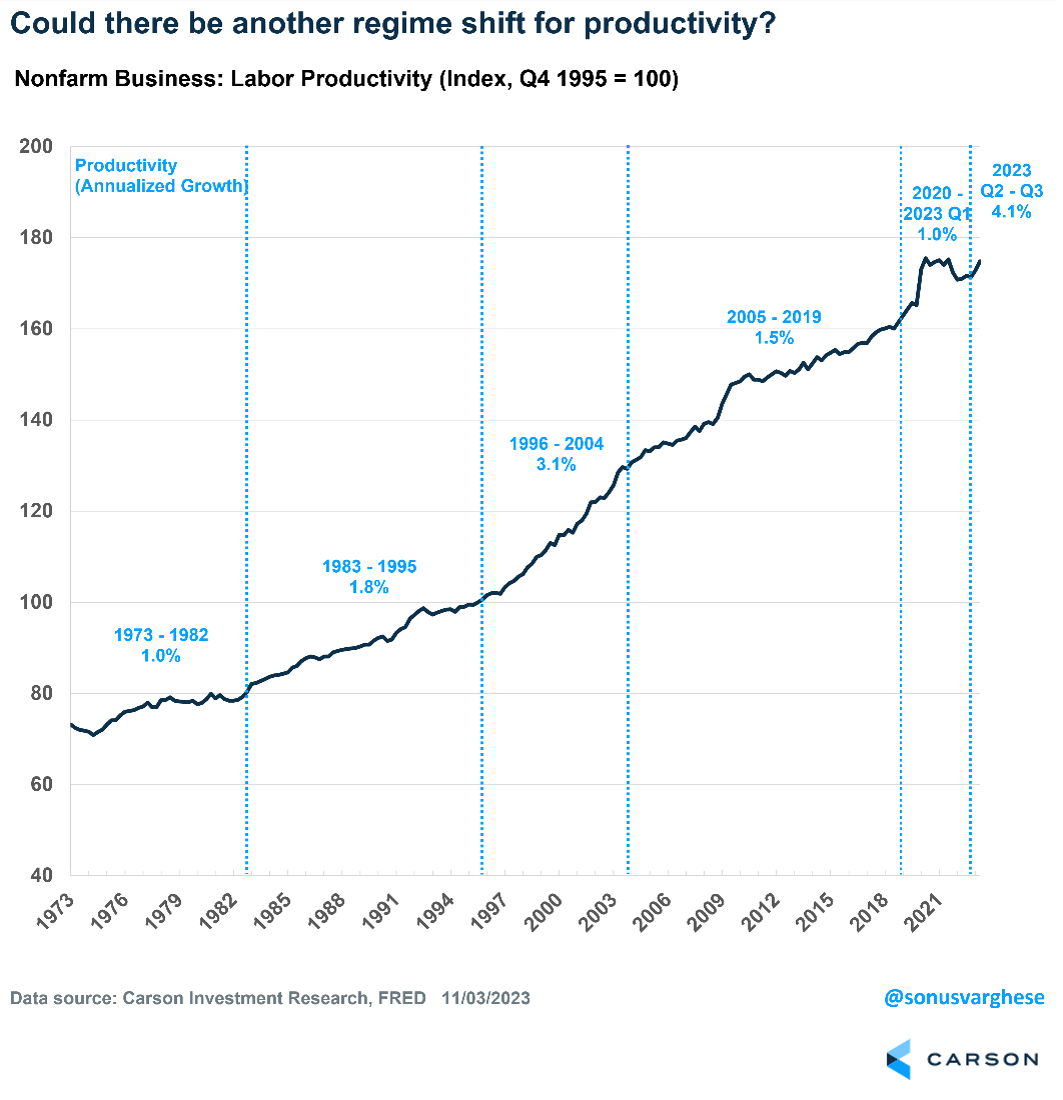

The relationship between wages, productivity, and inflation is best illustrated by reviewing historical examples. Here’s a chart of productivity starting in the 1970s, broken into several key periods.

Wage growth ran at an annualized pace of 8.9% between 1973 and 1982. However, that didn’t translate into productivity increases, which rose at an annual pace of just 1%. Instead, businesses passed on higher costs in the form of higher prices, and inflation averaged 8.2% a year! A significant reason for low productivity in the 1970s was the entry of a massive cohort of baby boomers into the workforce, and as mentioned above, hiring surges aren’t great for productivity.

Fast forward to 1996 and productivity began to advance. Wage growth ran at a 4.5% annual pace between 1996 and 2004. However, inflation averaged just 2.4%, translating to significant growth in inflation-adjusted incomes. This was because productivity climbed to a 3.1% annual pace during that period.

A Positive Feedback Loop: Policy and Productivity

As productivity boomed in the late 1990s, wages grew with low inflation. Crucially, periods like this can foster a positive feedback loop between policy and productivity. Strong productivity growth accompanied by low inflation can lead to more expansionary monetary policy. That can lead to greater investment and a tighter labor market with low unemployment and faster wage growth. That in turn can fuel further productivity gains and signal to the central bank that it can keep rates low.

This is essentially what happened in 1995, when Federal Reserve Chair Alan Greenspan chose to reduce interest rates despite strong wage growth. He bet that productivity would increase due to technological breakthroughs, and he was right. Expansionary policy also led to tight labor markets, which boosted productivity further.

We may be in a similar situation now, with tight labor markets leading to productivity gains rather than inflation. Of course, there is a risk that the reverse could happen, with overly tight monetary policy leading to falling investment, more unemployment, and slower wage growth, which could lead to lower productivity growth.

The good news is that the Powell-led Fed no longer seems to believe that a recession, and sharply rising unemployment, is required for inflation to fall. Fed members have watched inflation fall over the past year even as real economic growth has accelerated and unemployment has stayed low. Powell noted last week that there’s a risk of “doing too much,” and unnecessarily sending the economy into a recession. That is significant, as it means the Fed could ease policy if inflation falls substantially, which could happen if productivity runs strong.

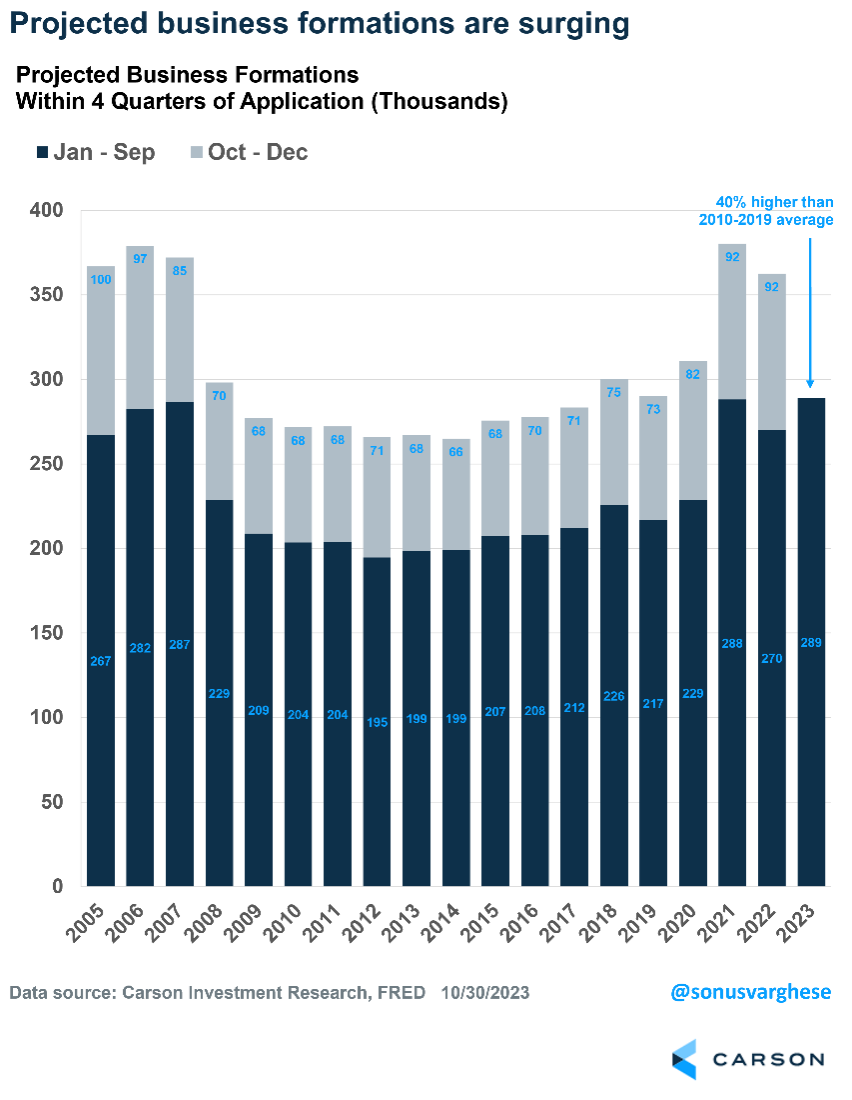

Another Positive: A Surge in Business Formation

Productivity is highest when a new business is formed and flattens as the business ages. Without new business formation, productivity is suppressed. Fewer startups in 2014 versus 1980 led to a 3.1% cumulative reduction in productivity for the U.S. economy. Business creation also provides employees opportunities to switch jobs for higher pay. To translate that, if this startup deficit hadn’t occurred, real median household income in 2014 would have been $1,600 higher, i.e., $66,500 instead of $64,900 and the cumulative effect on total wealth would be significantly higher.

Encouragingly, business applications are currently surging. The Census Bureau measures applications that have a “high propensity” of turning into a business with a payroll, as well as applications that include a first-wages-paid date on IRS forms. On a year-to-date basis (January-September), the Census Bureau’s projection of business formations is running 7% above the same period in 2022. It’s also 40% above the 2010-2019 average and 4% above the 2005-2007 average.

What About Artificial intelligence (AI)?

Artificial intelligence is certainly an x-factor with respect to productivity. As always, there’s a fear that automation will lead to job losses, but in reality AI can drive cost savings and free workers to do new tasks. As noted above, productivity growth tends to be accompanied by tight labor markets and higher wages, rather than the other way around.

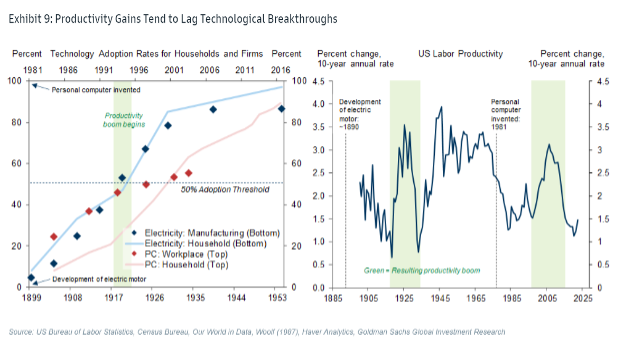

But it can take a while for technological breakthroughs to translate into productivity. The chart below from Goldman Sachs shows how productivity booms driven by milestone technologies, including motor vehicles and personal computers, lagged the initial innovation by more than a decade. They only showed up in the macroeconomic data after half of impacted businesses had adopted the technology.

Given the speed at which information travels these days, it may take less than a decade for AI adoption to show up in productivity data. Plus, unlike physical automation, AI is cognitive automation that can be rolled out via software. As this Brookings study points out, innovation can accelerate as cognitive workers not only produce their current output but also invent new things, engage in discoveries, and generate technological progress that boosts future productivity. In addition to research and development projects, managers may roll out new innovations into production activities across the economy. If cognitive workers are more efficient, they will accelerate technological progress and thereby boost the rate of productivity growth. If productivity growth was 2% per year, improved cognitive efficiency could boost it by 20% to 2.4% per year. That’s not much year to year, but these gains compound and the economy would be 5% larger after a decade.

All in all, there are many reasons to believe the economy could be at an inflection point. Much is riding on policy, and how the Fed navigates its policy path over the next year will be critical.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01979041_111323_C