Equities closed out April in strong form amid better-than-expected earnings and resilient economic data. The S&P 500 posted a gain of 1.6%, pushing its year-to-date gains to 9.2%. Not a bad way to start the first four months of the year, despite all the recession calls and the banking crisis of March.

- Sentiment is weak, but markets are rallying and consumers are spending.

- Investors are often told to “sell in May and go away.” But stocks don’t always sell off in May, especially in recent years.

- GDP growth was just 1.1% in the first quarter, but that masks underlying strength.

- Changes in inventories, which are usually volatile, pulled GDP down significantly.

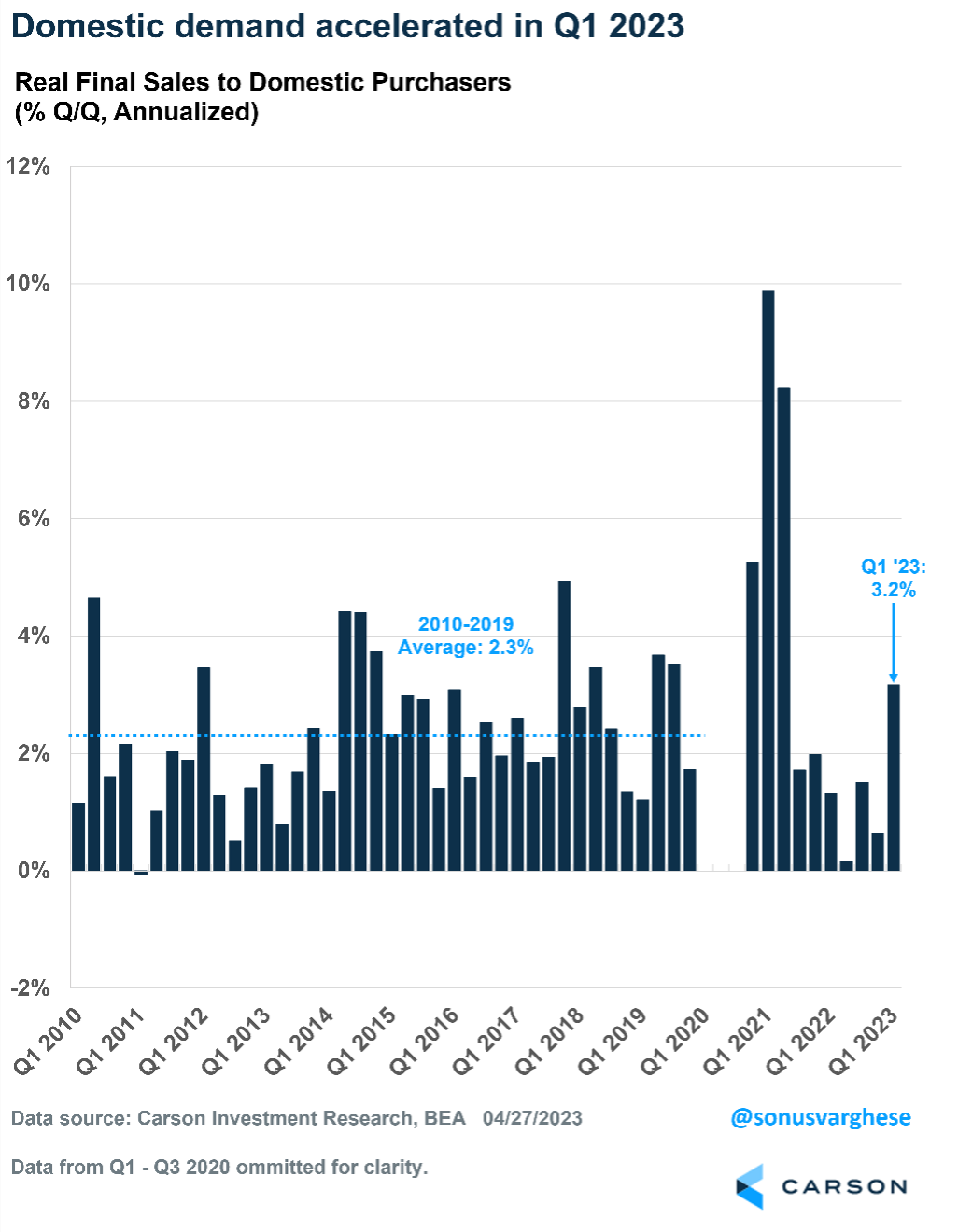

- Real demand rose 3.2% in the first quarter, the fastest pace of growth in almost two years.

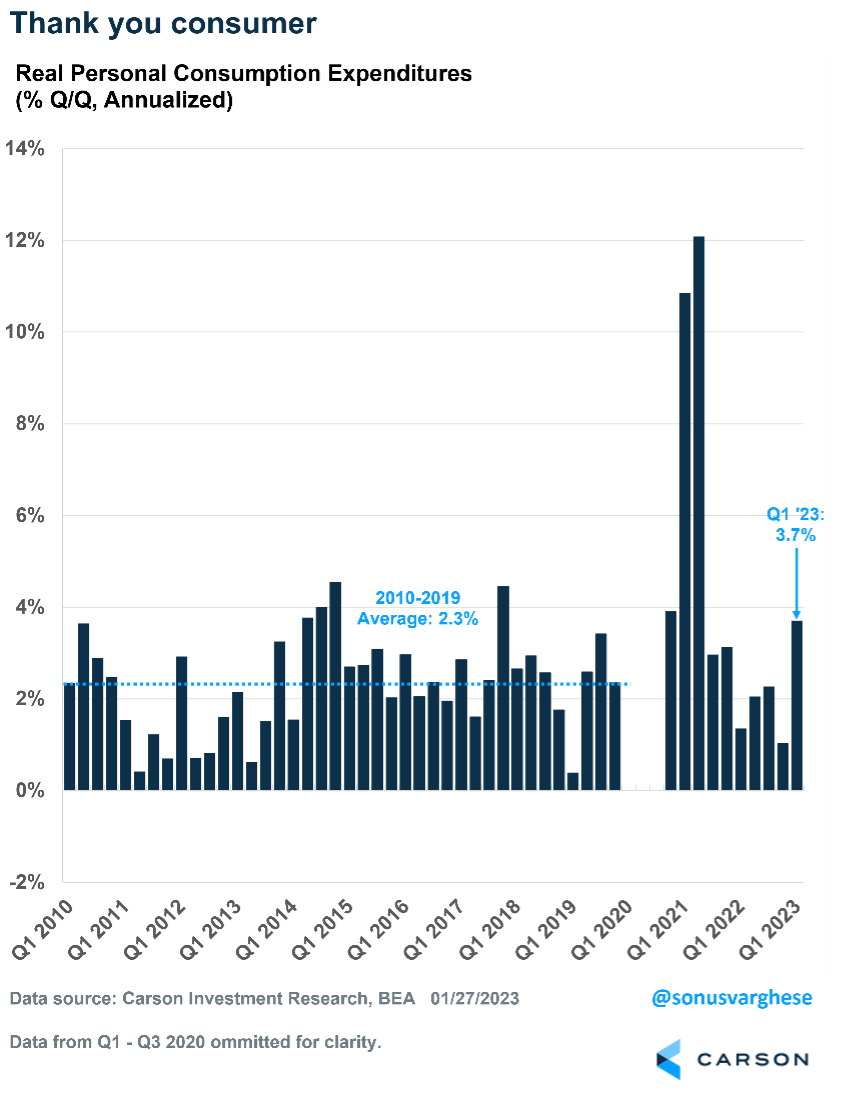

- Demand was powered by consumption and rising incomes.

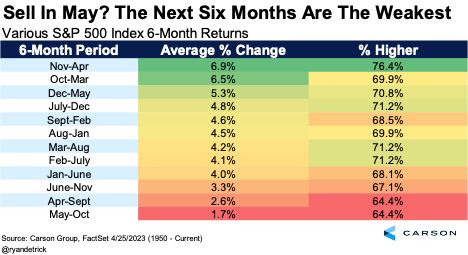

However, sentiment remains bearish. Also, May presents one of the most well-known investment axioms: “Sell in May and go away.” This gets a ton of play in the media, as the next six months are indeed the worst-performing period of the year. Plus, stocks did quite poorly last year during this timeframe, which only adds to the hype.

The thinking is investors are better off ignoring these six months. The S&P 500 is typically weak May through October, up only 1.7% on average and higher less than 65% of the time, making it indeed the worst investing period on average.

Of course, 1.7% is still a positive return. So, maybe we shouldn’t blindly go away? We believe there are several reasons not to fear these six months in 2023. Sure, more volatility and negative headlines could happen, but with overall market sentiment extremely bearish and the economy on firmer footing than most investors seem to think, we suggest using seasonal weakness as an opportunity to add to core positions.

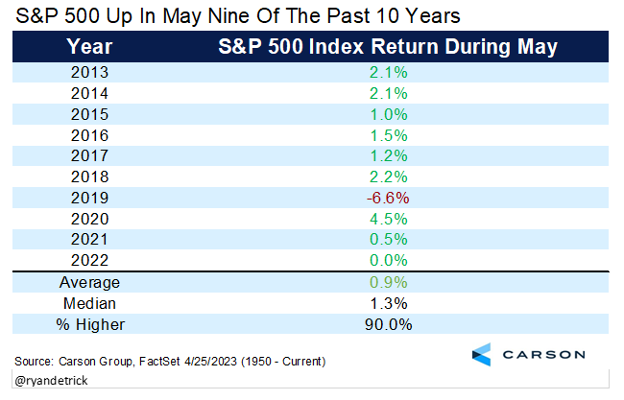

Also, here’s something most investors don’t know: May has been strong lately for stocks. Incredibly, it has been higher nine of the past 10 years.

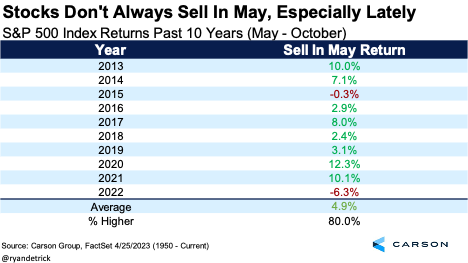

Last year was a great time to sell and go away during this historically weak period. But that isn’t always the case. Over the past decade, stocks have only fallen twice during this timeframe — last year and 2015. May-October has been up nearly 5% on average since 2013, far higher than its average 1.7% return since 1950.

Don’t Be Fooled by Headline GDP

The Bureau of Economic Analysis reported that the U.S. economy expanded by only 1.1% in the first quarter. That’s an annualized rate — the actual quarter-over-quarter increase is just under 0.3%. This was well below expectations for 1.9% growth.

More fodder for recession calls? The short answer is it shouldn’t be.

GDP can be broken down into five components:

- Personal consumption (68%)

- Business investment (13%)

- Residential investment, i.e., housing (4%)

- Government spending and investment (18%)

- Net exports, i.e., exports minus imports (-3%)

- Change in private inventories

The last two components are extremely volatile and can create significant swings in the headline data. Note that net exports are -3% of GDP because the U.S. exports less than it imports, and so net exports is negative.

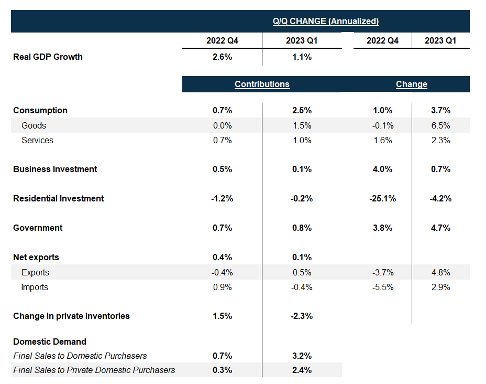

Here’s how the various components contributed to the headline number in the fourth quarter of 2022 and the first quarter of 2023. The last two columns show the pace at which they increased or decreased. As the chart shows, change in private inventories pulled GDP growth down by a whopping 2.3% in the first quarter.

Private inventories are the physical volume of inventories businesses maintain to support their production/distribution activities. These were more or less unchanged in the first quarter, but they increased significantly in the fourth. So “change in private inventories” showed up as a massive drag on GDP.

The good news is there is a measure of economic growth that excludes this volatility, which is shown in the last lines of the previous table. Domestic demand can be measured by “Real final sales to domestic purchasers,” which is simply the sum of the contributions from the top four components. And the private sector demand can be calculated by excluding government.

There Was No “Slowdown”

Domestic demand rose by 3.2% in the first quarter. That’s the fastest pace of growth since the second quarter of 2021. The average over the last decade (2010 – 2019) was 2.3%.

Domestic demand wasn’t boosted only by government spending, although this sector should not be ignored as it makes up close to a fifth of the economy.

Private sector demand rose 2.9% in the first quarter, which is the fastest pace since the second quarter of 2021.

Consumers Are Powering the Economy

Domestic demand was boosted by personal consumption, which surged at a 3.7% pace. Much of this came from a rebound in goods consumption, mostly thanks to more vehicle purchases. But even services spending, which makes up 45% of the economy, rose 2.3%.

For perspective on the consumption numbers from the first quarter, the pace of growth was a lot faster than the 2.3% average experienced during the last decade and the fastest since the second quarter of 2021. However, consumption in 2021 was boosted by stimulus checks.

What’s driving strong consumption now?

- Strong employment

- Lower inflation, especially gas and food prices, which is boosting real incomes, i.e., incomes adjusted for inflation

What Next?

All the above data is for the first quarter, and we’re already a month into the second. It’s hard to imagine consumption and domestic demand growing at the torrid pace of the first quarter. However, for those predicting a recession it might be difficult to identify what could lead to a crash in employment or higher inflation going forward.

The latest employment news is positive. Initial claims for unemployment benefits dropped last week, from 246,000 to 230,000. This means fewer workers were laid off and filing for benefits. Even continuing claims, which represents the total number of people continuing to receive unemployment benefits, were unchanged at about 1.86 million.

Beyond the numbers, what matters is the trend. And we’re not seeing a pickup in initial or continuing claims. In fact, the current levels are in line with those seen prior to the pandemic when employment was strong. Of course, with job growth already hitting 1 million plus in the first quarter, and the unemployment rate close to 50-plus-year lows, I think it’s safe to say we have a strong labor market.

Another potential positive going forward: housing. Residential investment has dragged on GDP growth for eight straight quarters. But as we wrote last week, we see relief coming from this sector of the economy, which would be more than welcome.

We’ll continue to track the data, including inflation and payrolls. Those will tell us a lot about how things are looking in the second quarter and, just as importantly, what that means for monetary policy.

The other side of strong domestic demand is that it’s hard to imagine Fed officials reviewing the numbers and thinking their job is done and it’s time to cut rates. But we’ll see.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01749933