Founded in 1983, Silicon Valley Bank’s parent company, SVB Financial, announced on Wednesday it had sold $21 billion in assets to raise cash and was taking a $1.8 billion loss while also trying to raise capital. Due to dwindling deposits and losses in its holdings, the bank was forced to sell to shore up its books. As a result, there was a classic run on the bank, as customers demanded their money back. In less than 48 hours, the 16th largest bank in the U.S., with $209 billion in total assets as of the end of 2022, was gone. In fact, it is estimated customers tried to withdraw $42 billion on Thursday alone, about a quarter of the bank’s overall deposits.

- The nation’s 16th largest bank went under in 48 hours, creating mass confusion and a sell-first-ask-questions-later mentality.

- In our view, the fallout will be contained to Silicon Valley Bank and will not spread to other banks.

- The Federal Reserve has stepped in to prevent a similar situation at other banks and avert a crisis across the entire banking industry.

- Meanwhile, the labor market remains strong, no two ways about it.

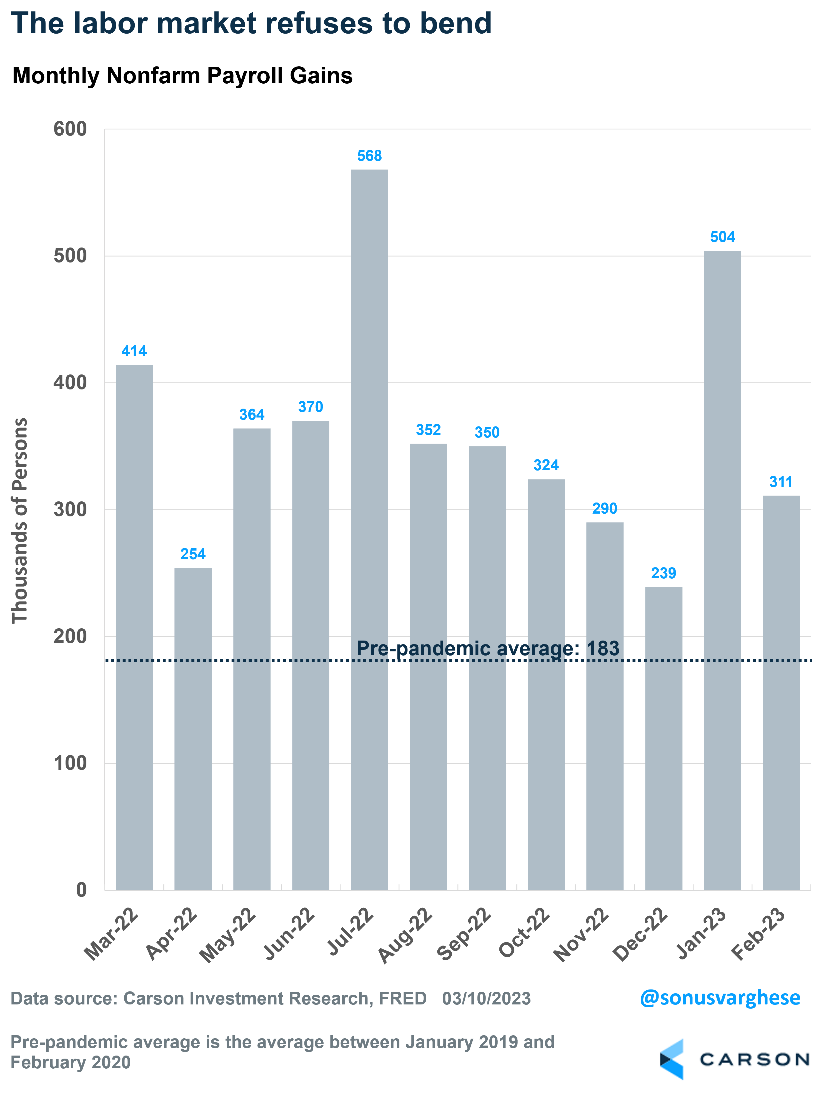

- Payrolls grew by 311,000 in February, continuing the recent trend of strength.

- The unemployment rate rose to 3.6%, but that was because more people started looking for jobs.

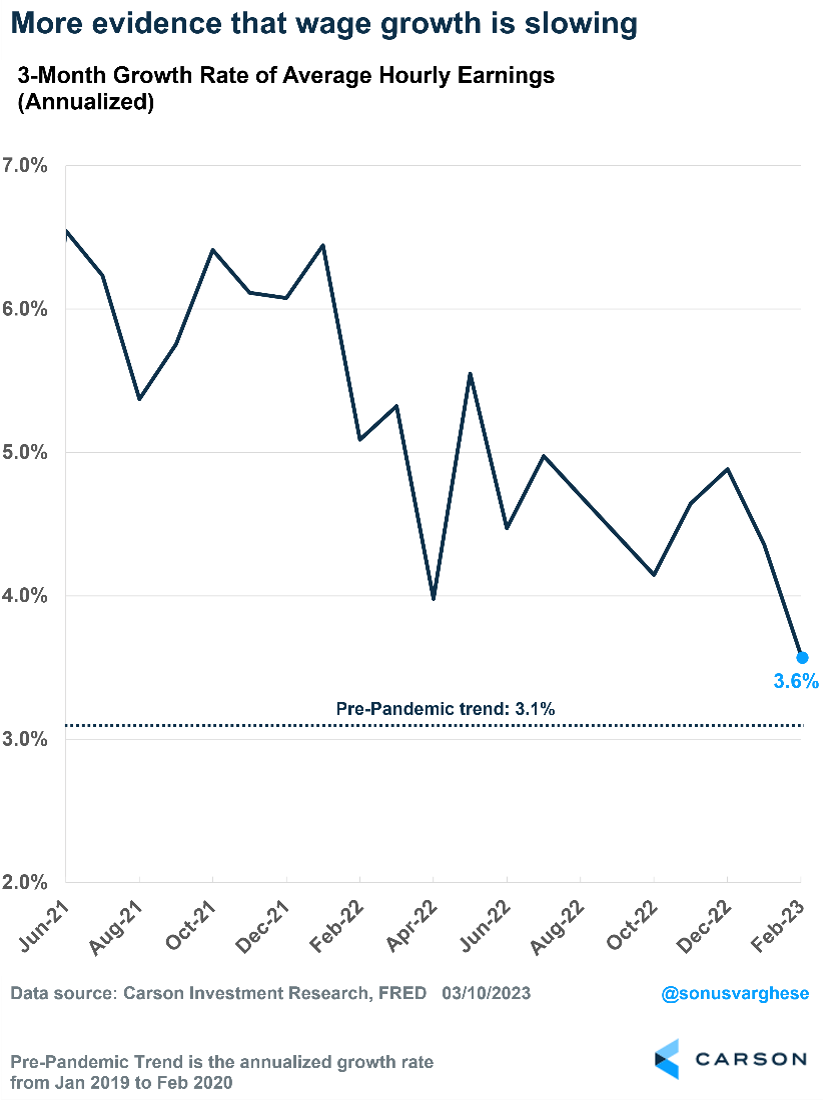

- Wage growth continues to decelerate, which should ultimately translate to lower core inflation.

- However, Fed Chair Jerome Powell injected uncertainty into the markets last week with his comments before Congress.

As a result of the flood of withdrawals, the bank had a negative cash balance of close to $1 billion and couldn’t cover its payments, so the FDIC took over on Friday morning.

Why did this happen to SVB? The bank was quite unique in that it focused on technology and health care companies, along with venture capital and startups. In fact, it provided almost half of the financing for U.S. venture-backed technology and health care companies. So, whereas traditional banks had various types of customers, SVB’s client base was quite lopsided. This worked great when tech and startups soared from 2015 until 2021, but that all changed in 2022.

The technology sector was hit hard by rising interest rates last year. Instead of depositing money in the bank, tech companies took out more and more to cover their bills. SVB also had enormous unrealized losses in its portfolios of mortgage bonds and Treasury bonds. Combined, it was the perfect cocktail for trouble.

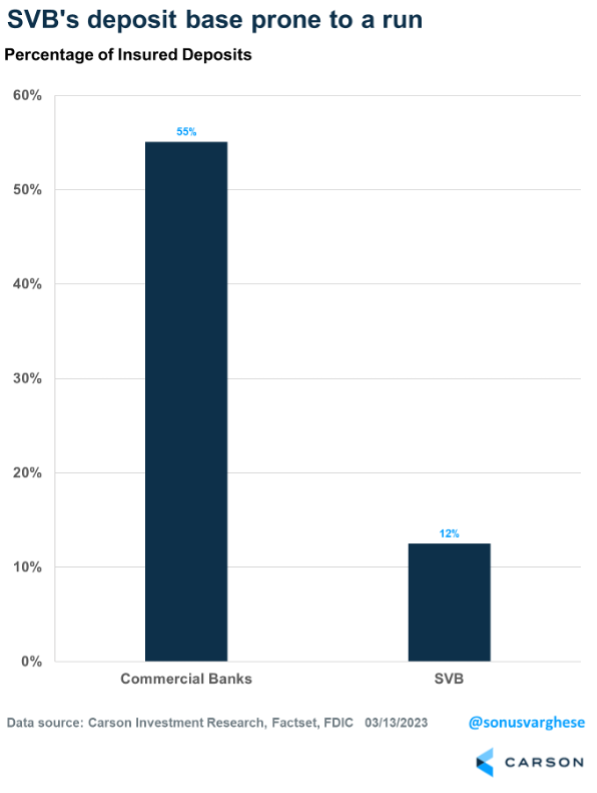

Was this the first domino to fall? Silicon Valley Bank was unlike nearly any other bank, and its portfolio set it up for distress. Bank accounts are insured up to $250,000, according to the FDIC, but most of the accounts at SVB were well above this important threshold. That meant when trouble came, investors wanted their money back fast. In fact, only 12% of its overall deposits were insured, compared with the average commercial bank’s rate of 55%.

Respected Wells Fargo analyst Mike Mayo said the issue was the diversity of deposits, with most customers being venture-capital firms. Larger banks won’t be as pressured. “To us, the larger the bank, the more diversified the funding,” Mayo explained. “This is part of the test that the largest banks, i.e., the ones that caused the Global Financial Crisis, are today the more resilient portion of both the banking and financial systems.”

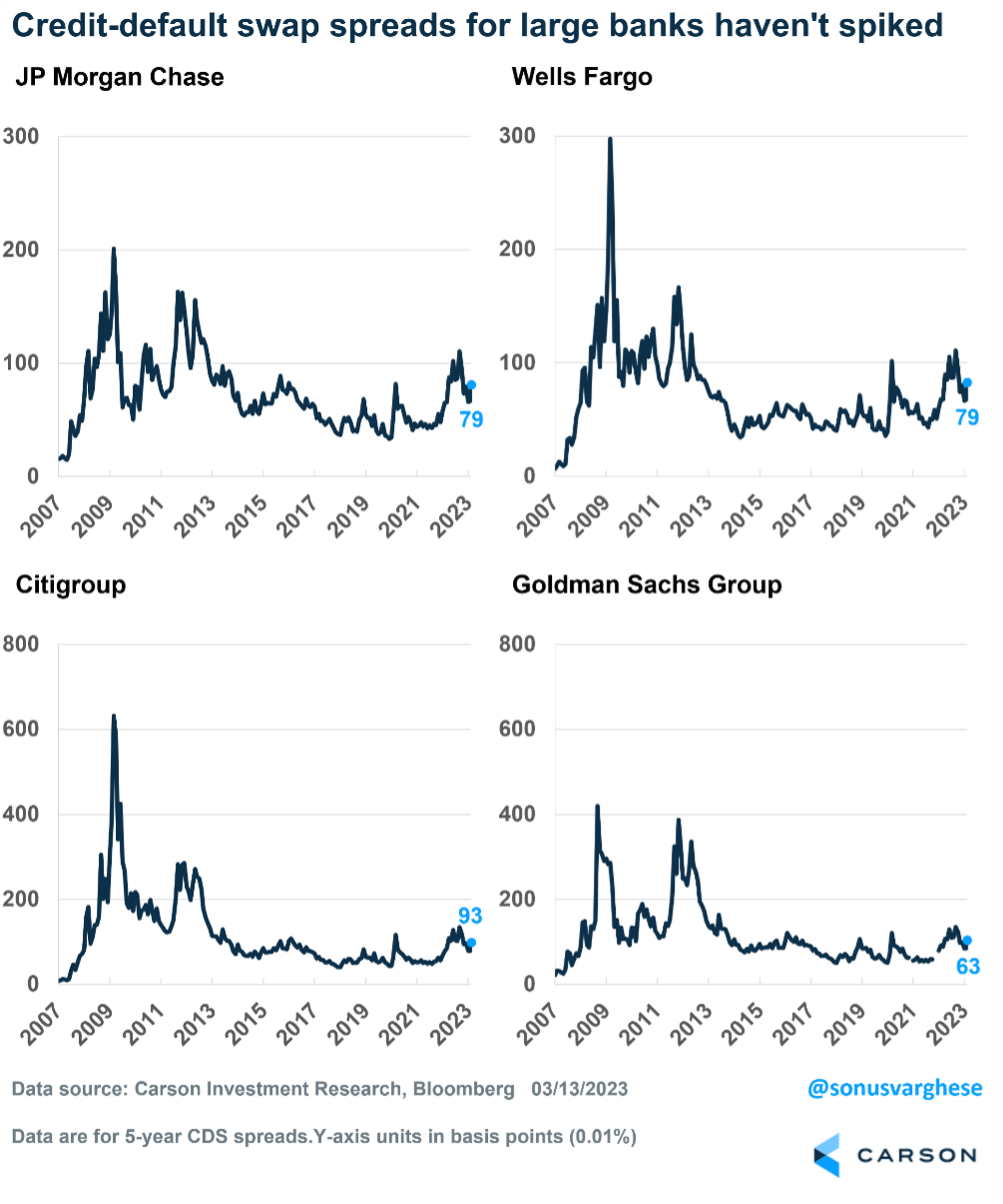

Although bank stocks and the financial industry in general had a historically bad week, it was worthwhile to note that credit markets remained calm. In fact, credit default swaps of large banks didn’t show any signs of stress, suggesting things are contained as of now. Additionally, the U.S. dollar weakened late in the week. Historically, the U.S. dollar finds a bid under times of extreme stress.

We will continue to monitor these events closely. But as of now, the fall of SVB does not appear to be the first domino before another major financial crisis.

The Fed Steps In To Prevent a Broader Crisis

Late Sunday evening, the Federal Reserve, Treasury, and FDIC issued a joint statement that all deposits at SVB will be protected. At the same time, shareholders and some debtholders will not be protected.

The Fed is making available additional funding for banks across the U.S. to make sure they can meet all the needs of their depositors. This is a massive step and will help banks avoid the situation that happened at SVB. It will also bolster confidence in the banking system and prevent contagion.

Not a moment too soon, especially since the economy can do without a wrecking ball.

Payrolls Strong But Unemployment Rises: All Mixed Up

Another month, another solid employment report. Employment rose by 311, 000 in February, on the back of 504,000 in January and 239,000 in December. It’s certainly been a warm winter. This is the labor market that refuses to give in, despite the Fed throwing almost 500 bps (5%-points) of rate hikes at the economy and gearing up for more.

But the Unemployment Rate Rose…

Yes, the unemployment rate rose to 3.6%, up from 3.4% in January. However, that was entirely for positive reasons.

The unemployment rate, as the Bureau of Labor Statistics measures it, is the number of people unemployed who are looking for work divided by the size of the labor force. Last month, the number of unemployed people looking for work rose by about 240,000. However, that’s because 419,000 people “entered” the labor force, i.e., started looking for work. That’s a sign of a healthy labor market. People will start looking for work only if they think they can get a job.

The labor force measure has issues related to how participation is measured. It counts someone as being in the labor force only if someone is looking for work. But a lot of people may not do so for any number of reasons, including not feeling confident in the job market, or non-economic reasons, such as not having access to childcare. The measure also can fall over time because of retiring baby boomers.

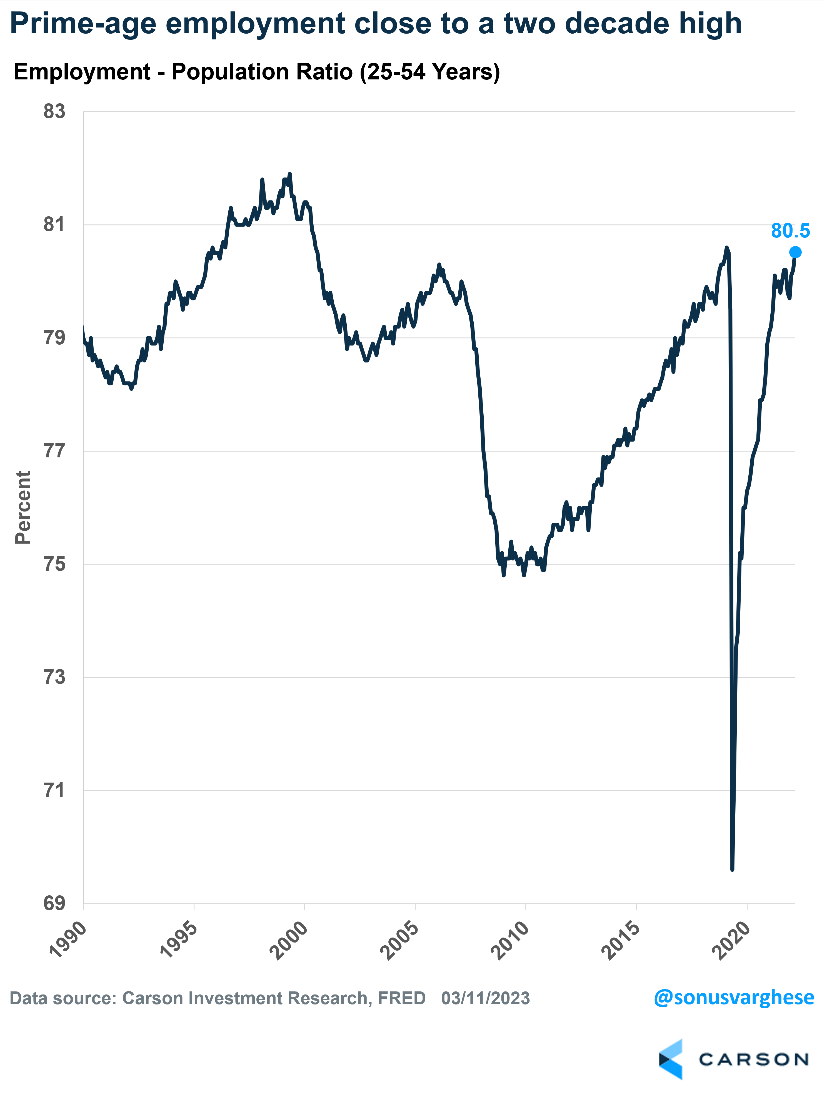

One way to get around these issues is to look at the employment-population ratio for prime-age workers, i.e., workers aged 25-54 years. This measures the number of people working as a percentage of the civilian population. Think of it as the opposite of the unemployment rate, and because we use prime age, we get around the demographic issue as well.

The good news is the prime-age employment-population ratio just hit 80.5%, which is close to the highest level we’ve seen in a couple of decades.

It helps to recall that we just had a multi-generational black swan event in the form of a pandemic. But once everything reopened, the expectation was the economy would bounce back immediately. Several areas did, including GDP, employment, and consumption.

However, a lot of people left the labor force amid the pandemic. Now people are flowing back into the labor force monthly and finding jobs quickly. Just over the past six months, 1.5 million more people have come into the labor force as prospects for finding a job improve.

Make no mistake, this is a really strong labor market.

Is the Labor Market Too Strong?

It’s weird to even ask that question, but it matters for the Fed. In its model for the economy, the Fed believes a tight labor market results in stronger wage growth, which drives demand higher and pushes up prices and inflation.

Hopefully the Fed can rest easy on that front. Average hourly earnings rose just 0.2% in February. Over the past three months, wages have grown at an annualized pace of 3.6%, well below the 6%+ pace we saw last year. It’s getting very close to the pre-pandemic pace of 3.1%.

The big question is whether the Fed buys this narrative. Fed Chair Jerome Powell’s comments last week before Congress, for his semi-annual testimony on monetary policy, did not inspire confidence. It looks like a string of hot economic data has left Fed officials questioning their decision to ease the pace of rate increases from 0.5% to 0.25% (as of February) and wondering if they should move that back up to 0.25% at their March meeting. At this point, markets think the outcome is more or less a coin toss, which is not great as Powell simply injected maximum uncertainty into the markets.

Beyond the Fed’s March meeting, the labor market remains strong. This means the economy remains strong, and that’s encouraging for markets. However, it also means the Fed is likely to keep interest rates higher, for longer.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01688051