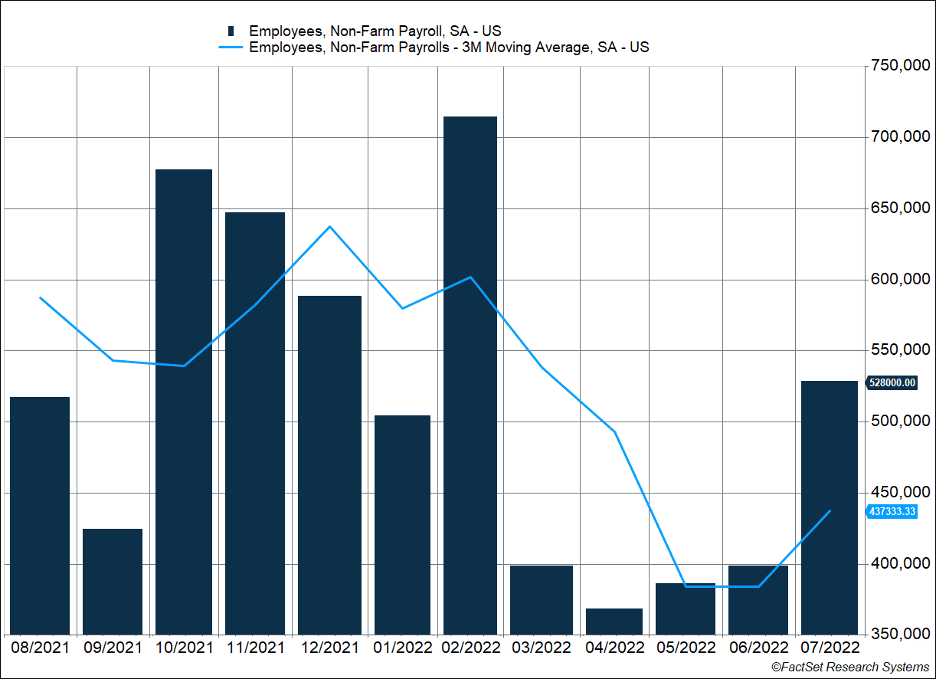

The U.S. job market didn’t get the message it was supposed to slow down. The establishment survey estimated 528,000 new jobs were created last month. Every employment sector experienced growth, although services and government hiring accounted for 87% of new jobs.

Key Points for the Week

- The U.S. economy created 528,000 net new jobs in July, more than doubling expectations for a 250,000 increase.

- Unemployment reached the pre-pandemic low of 3.5% last month, while wages rose 0.5%.

- Earnings are expected to have grown approximately 6.7% in July, but without energy stocks earnings have declined.

A couple pre-pandemic milestones were reached. There are now more people employed in the U.S. than prior to the pandemic. Unemployment also dipped 0.1% and reached the pre-pandemic low of 3.5%. Getting all these people to take jobs didn’t come cheap. Private sector wages increased 0.5% in July, which is faster than the economy can sustain without pushing inflation higher.

S&P 500 earnings are expected to rise 6.7%. Energy companies have experienced rapid earnings growth as energy prices have climbed. Without energy growth, S&P 500 earnings would have dropped. The financial sector contributed most to earnings weakness, with approximately 25% of the S&P 500 still to report.

Markets held on to the previous week’s gains, while faster growth pressured bonds. The S&P 500 added 0.4% last week. The global MSCI ACWI edged 0.3% higher. The Bloomberg Aggregate Bond Index declined 1.0%. The Consumer Price Index leads the list of economic data released this week. Markets will likely focus on core inflation as energy price declines are expected to help rein in July’s headline inflation.

Figure 1

Jobs Data Show Underlying Economic Strength

The U.S. employment report indicates the U.S. economy remains strong despite much speculation to the contrary. The economy added 528,000 new jobs last month, according to the establishment survey. Rather than job growth slowing, the survey indicated the economy added the second most new jobs this year. With the gains, the economy has added 3.3 million jobs in 2022 and 1.3 million in the last quarter. The problem may be the economy remains too strong, not too weak.

The underlying data showed the gains were broadly based. Every industry increased employment. Health care and social services, leisure and hospitality and professional and business services all added close to 90,000 jobs. Government hiring, in advance of a new school year, rose 57,000. With the gains, employment reached the level it was before the pandemic, and the unemployment rate fell back to 3.5%, its pre-pandemic low.

One area that hasn’t reached previous levels is labor force participation. The overall labor force participation rate fell to 62.1% in July. When only prime-age workers 25-54 are included, that number rises to 80.0%. Prime-age participation is close to the pre-pandemic record but not quite there. Because supply challenges are contributing to inflation, getting people back to work can help fill key roles and cap wage pressures.

Fighting inflation will mean getting wage inflation under control. Prior to the pandemic, aggregate payrolls rose about 5% per year. Increased average hourly earnings accounted for most of the gains, and a significant minority resulted from new jobs being added to the economy. In the last 18 months, yearly payroll increases have averaged around 10%, with gains roughly split evenly between higher earnings and new jobs.

The strong jobs data mean the chief worry has swung from recession back to inflation. As we noted last week, two negative quarters is a popular definition of a recession. The National Bureau of Economic Research uses six primary indicators to determine if the economy is in a recession. Only one of those is negative: real wholesale and retail sales. The nominal level of sales remains strong, but high inflation has pushed that indicator negative. A measure of real income excluding government payments to individuals is neutral. The other four indicators — total employment, employment level, real personal consumption, and industrial production — are all positive.

For inflation to start declining, wage gains will have to slow. Renewed concerns about inflation mean the Federal Reserve may do more than expected. Prior to the jobs data, markets reflected a 66% chance for a 0.50% rate hike in September and a 34% chance of a 0.75% hike. After the jobs data, odds swung to 70% expecting a 0.75% increase and only 30% predicting 0.50%. Strong economic data mean the market expects the Fed to do more to tame inflation.

The CPI report this week will be the next big indicator of current economic conditions. Core inflation excludes food and energy, and many believe that reflects the underlying trend in inflation better than headline data. Headline CPI, which has been higher than the core rate, should be lower than core inflation. In July, energy prices dropped, and that should help temper headline inflation. We will be watching core inflation to see if lower energy prices spilled over into core inflation categories and the rapid inflationary pressures start moving the other way.

Keep in mind it will be more than a month before the next Fed meeting. Another employment and CPI report will be released before then. It also means the Fed’s tightening strategy will have another month to work itself into the economy. A rate hike in September seems nearly certain. The level will depend on how future data affect the overall outlook. Expect volatility to remain elevated and more swings between recession and inflation concerns. There is a lot to think about in the current market, and as we’ve learned the market is almost always worried about something.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

BLOOMBERG U.S. AGGREGATE BOND

The Bloomberg US Agg Total Return Value Unhedged, also known as “Bloomberg U.S. Aggregate Bond Index” formerly known as the “Barclays Capital U.S. Aggregate Bond Index”, and prior to that, “Lehman Aggregate Bond Index,” is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS and CMBS (agency and non-agency).

Compliance Case # 01453039